Ofgem has recently released the updated tariffs for the commercial RHI scheme. These changes have taken place primarily due to the annual inflation of the RHI, the third increase since the scheme was launched. However, changes have also taken place in response to increasing uptake of the scheme, particularly in the small and medium biomass projects.

The inflation of the tariff, this year by 2.7%, affects those already in receipt of payments from Ofgem as well as installations that will become accredited after April 1st 2014.

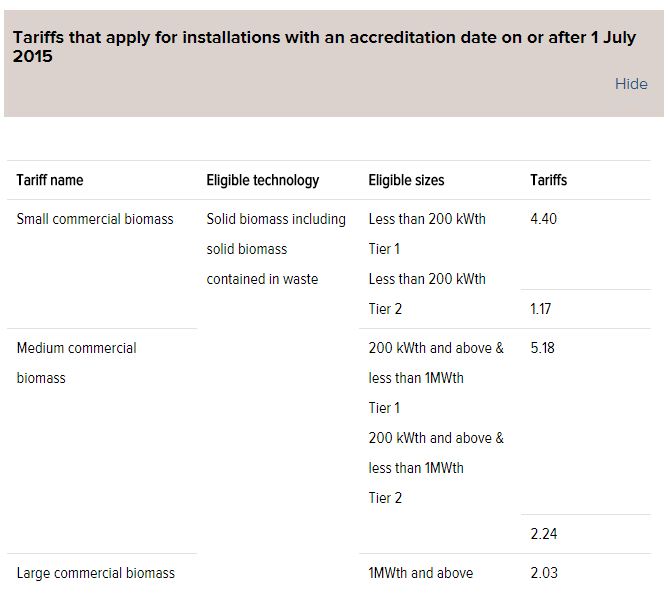

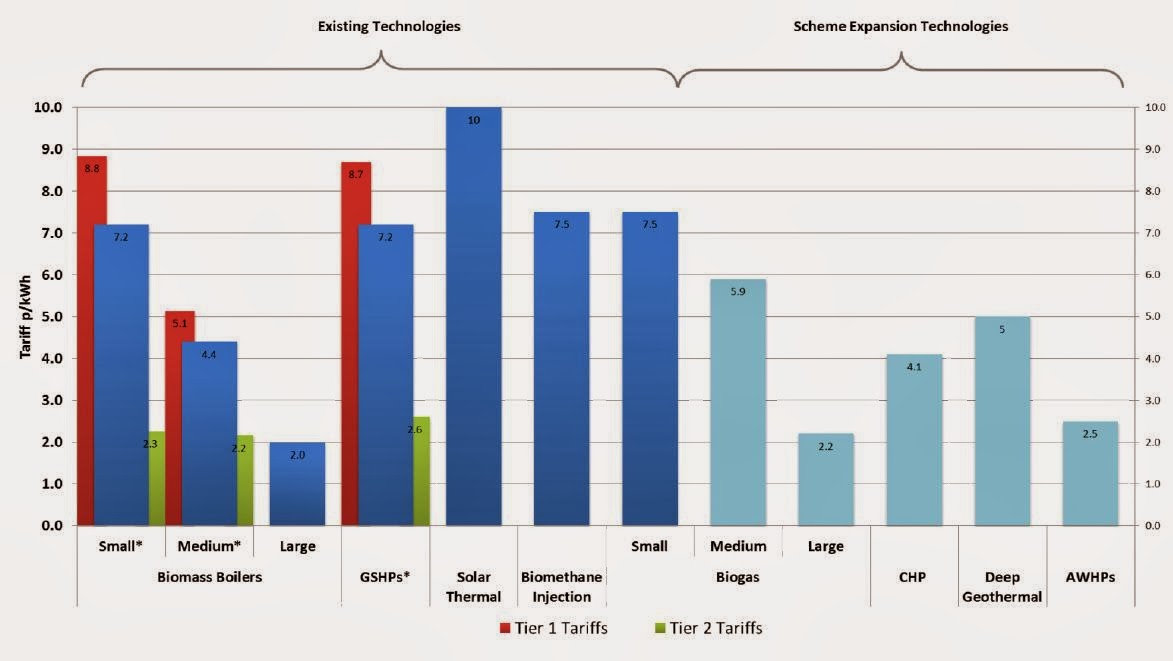

The following table focuses on the biomass tariff. For example, for boilers sized up to 199 kW the Tier 1 tariff has increased from 8.6 p/kWh to 8.8 kWh (the Tier 2 tariff from 2.2 to 2.3 p/kWh). The last column in the following table shows the updated tariff (from 01/04/2014).

Whilst these changes are not earth shattering the increases help to further enhance the economics of RHI accredited biomass boilers. For example, the annual RHI payment for a 199 kW boiler serving a 280,000 kWh heat load would increase by around £500 per year.

The only downside to these changes is the reduction in the tariff for medium-scale biomass boilers that were accredited after July 1st 2013 (Tier 1 down to 5.1 p/kWh and Tier 2 remains at 2.2 p/kWh). This change indicates that degression has taken place in the medium category due to rising uptake of the RHI in this category.

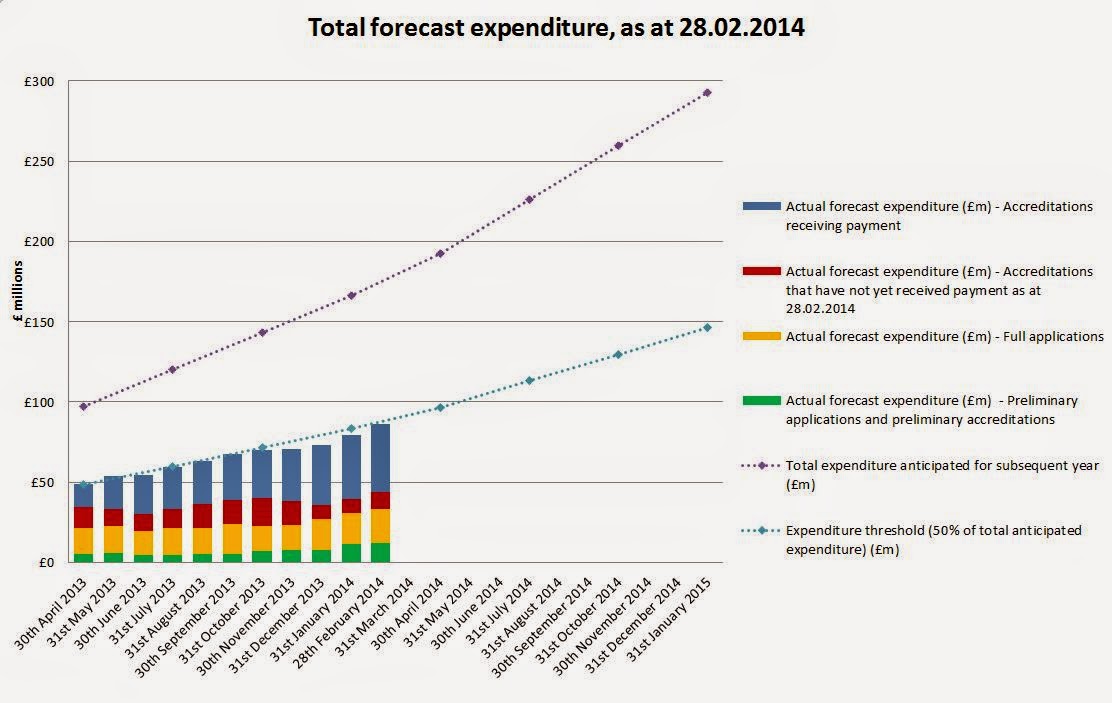

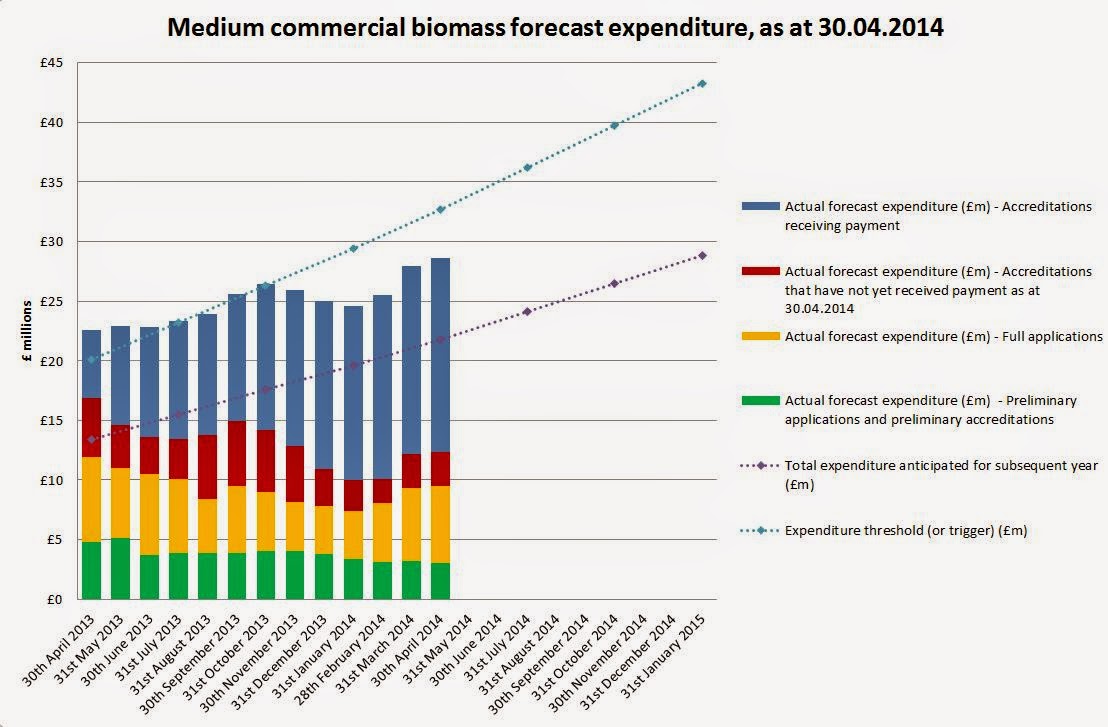

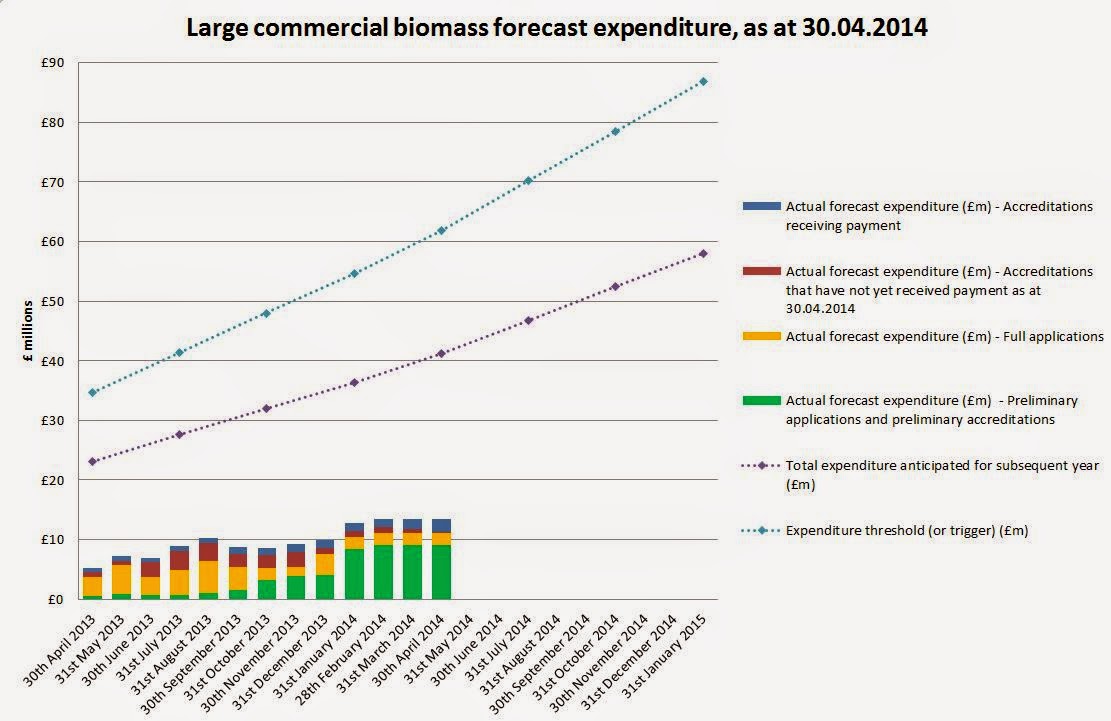

Whilst the overall expenditure for the RHI is proceeding according to forecast it is clear that the small biomass category has seen the largest increase in expenditure.

Ofgem states that:

"Forecast spend over the next 12 months for small commercial biomass is £44.4m. This means that estimated spend for this technology is already £10.4m above its 30 April 2014 individual technology trigger point of £34.0m. This increases the possibility of a reduction to this tariff in the next quarter. However, this would only occur if next quarter’s 50% trigger for the scheme as a whole of £96.4m was also exceeded, which would require a £10.1m increase in total expenditure over March and April."

Other developments include:

- Forecast spend over the next 12 months for medium & large commercial biomass has increased by 4% and 6% respectively.

- Forecast spend for small heat pumps has seen a significant increase of 25% in the last month.

- Forecast spend for all other tariff categories have seen little to no activity this month and remain considerably below their individual tariff triggers for the next quarter.

The future risk of degression is summarised by Ofgem as follows:

"Whether any reductions occur next quarter depends on how well the scheme overall, and each technology tariff, performs during March and April and whether total scheme spend grows by £10.1 million in that time. An increase of this size would occur if the scheme was to continue to grow at the rate we have seen this month which would cause the 50% total scheme trigger of £96.4m to be hit. DECC will receive the data needed to make this forecast in May, and will publish the next quarterly degression announcement by 1 June 2014, following which, any reduced tariffs would come into effect from 1 July 2014."

The Department of Energy and Climate Change has announced changes to the RHI tariffs for biomass in both the domestic and non-domestic schemes.

The Department of Energy and Climate Change has announced changes to the RHI tariffs for biomass in both the domestic and non-domestic schemes.

Ofgem has revealed more detail on how it intends to roll out and implement sustainability requirements for biomass fuels.

Ofgem has revealed more detail on how it intends to roll out and implement sustainability requirements for biomass fuels.

The only downside to these changes is the reduction in the tariff for medium-scale biomass boilers that were accredited after July 1st 2013 (Tier 1 down to 5.1 p/kWh and Tier 2 remains at 2.2 p/kWh). This change indicates that degression has taken place in the medium category due to rising uptake of the RHI in this category.

The only downside to these changes is the reduction in the tariff for medium-scale biomass boilers that were accredited after July 1st 2013 (Tier 1 down to 5.1 p/kWh and Tier 2 remains at 2.2 p/kWh). This change indicates that degression has taken place in the medium category due to rising uptake of the RHI in this category.

Public Grants

Public Grants

Remember the date - 24th September

Remember the date - 24th September