The Department of Energy and Climate Change has announced changes to the RHI tariffs for biomass in both the domestic and non-domestic schemes.

The Department of Energy and Climate Change has announced changes to the RHI tariffs for biomass in both the domestic and non-domestic schemes.Domestic RHI

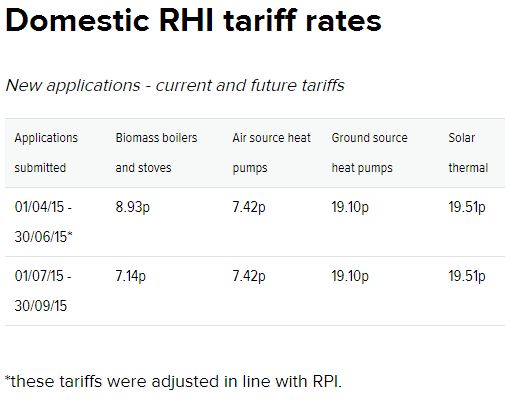

DECC announced on 29 May 2015 that the degression ‘super trigger’ for domestic biomass had been passed.

This means that the current biomass tariff of 8.93p per kilowatt hour will be reduced by 20% to 7.14p per kilowatt hour for all new applications made from 1 July 2015. The new tariff table is shown below.

To calculate the impact of this change simply multiply the tariff by the kWh total for space heating and hot water on your EPC (e.g. 15,000 kWh x 0.0893 = £1,339 per year for seven years).

The tariffs for domestic air source heat pumps, ground source heat pumps and solar thermal are not affected by the 1 July 2015 degression. Legacy applicants are not affected by degression.

Non-Domestic (Commercial) RHI

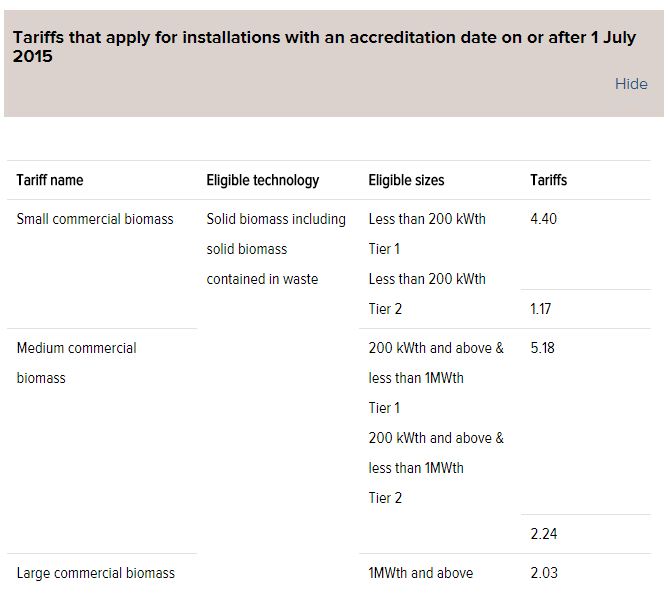

DECC has also announced a 25% reduction to the small commercial biomass tariff for the quarterly period starting on 1 July 2015.

This is a fairly significant reduction that will affect the economics of schemes up to 199 kW - particularly those involving wood pellets and the replacement (partial or full) of mains gas.

Nevertheless, a subsidy is still a subsidy and 4.4 p/kWh is still a positive contribution.

The risk with this degression is that larger boilers will be installed to gain the 'medium' tariff. Whilst tempting this is likely to be a false economy as an over-sized boiler will be used less and is likely to have worse overall efficiency (it may well cost more as well).

Our advice would be to size correctly and be satisfied that a subsidy is still available.

If your sub-200 kW project is nearing completion then you have only a few weeks left to commission and apply in order to gain the current tariff (5.87 p/kWh).

More details can be found on the Ofgem website.