DECC has launched a consultation on possible approaches to cost control for the RHI.

The document focuses on the amount of notice that would be provided and is largely informed by the difficulties that were caused by short-notice changes to the Feed in Tariff. The proposals range from one month, one week and no notice.

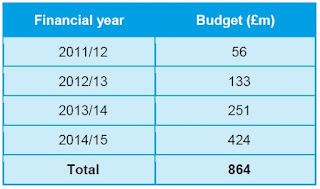

The document also clarifies the structure of the RHI budget. It is interesting to note that each year has a fixed budget and any underspend will not be carried over to the next year.

As of 18th March 2012 298 applications hd been received, of which only 11 have been accredited. Based on the current level DECC expects that spend in 2011/12 will be approximately £2m, which is somewhat short of the £56m allocated to 2011/12 (although this includes £25m for RHPP Phase 2).

Based on this uptake DECC suggests that the proposed interim cost control measure would not be needed and suspension would not occur.

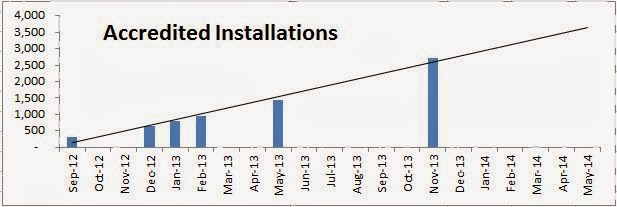

However, based on our recent interaction with installers there is likely to be a step-change in the number of new applications over the next quarter as both new systems and post July-2009 projects are submitted.

|

| Annual RHI budget (Source: DECC) |

Predicted budget allocations for 2012/13 are:

- £15m - from

installations already accredited

- £40m - new installations

coming on stream

The main points from the consultation are as follows:

The Renewable Heat Incentive continues to be a top priority

for Government as a means to reduce our carbon emissions and because it is

central to delivering our strategic framework for heat. It is therefore

essential that the RHI policy is sustainable and that we have the ability to

ensure that year to year spending does not exceed available funding.

This consultation sets out a proposed interim cost control

measure that would suspend the RHI until the next financial year should

estimated spending reach a level where the budget could be breached.

Only new applications would be affected. Accredited

installations already receiving the RHI tariff from Ofgem would continue to

receive that tariff. Applications submitted to Ofgem prior to the suspension

would be processed as normal.

Current application levels are low relative to the available

budget and if these levels were to continue the proposed interim cost control

measure is unlikely to be needed. However, there is a high degree of

uncertainty about how the market will respond and we need to be prepared for

unexpected changes in uptake. Having this interim approach set out in advance

will ensure that Government is able to respond quickly if required and that

stakeholders will be sighted on future action.

The proposed circumstances under which suspension would

occur will be specified in the RHI regulations and will include a predetermined

trigger that would set off suspension and a fixed notice period before the

suspension begins.

We intend to frequently publish the data being used to

monitor progress towards the trigger. This will allow the market to make

informed decisions about the likelihood of suspension.

We are proposing this policy as an interim measure. Over

summer we plan to consult on a longer-term flexible degression-based mechanism

which would automatically reduce tariffs should spending against the overall

budget or deployment of certain technologies exceed forecasts.