As the first anniversary of the Renewable Heat Incentive approaches we thought we would take a quick look at progress to date.

In terms of overall numbers the results are modest. In England the number of accredited installations is 406. Of these 358 (88%) are for biomass boilers, 25 (6%) for solar thermal and 19 (5%) for ground source heat pumps.

|

| Data Source: Ofgem, 19/11/2012 |

The relatively low uptake in the solar thermal and ground source categories is interesting and suggests that these technologies are yet to find traction in commercial situations. This low uptake may also be due to the popularity of the Feed in Tariff which has probably diverted attention towards solar PV, particularly where biomass is not an option.

The results also show that the RHI tariff is yet to be used for deep geothermal, municipal sold waste or bio-methane installations. As these technologies are often used at larger scales it may be that other incentives are being favoured, such as the Renewables Obligation Certificate (ROC). Another factor is the high capital cost of these technologies which undoubtedly take longer to plan and finance. Uptake of the RHI might therefore pick up in time, but in the absence of any other information from DECC (e.g. pre-accreditation) it is hard to tell.

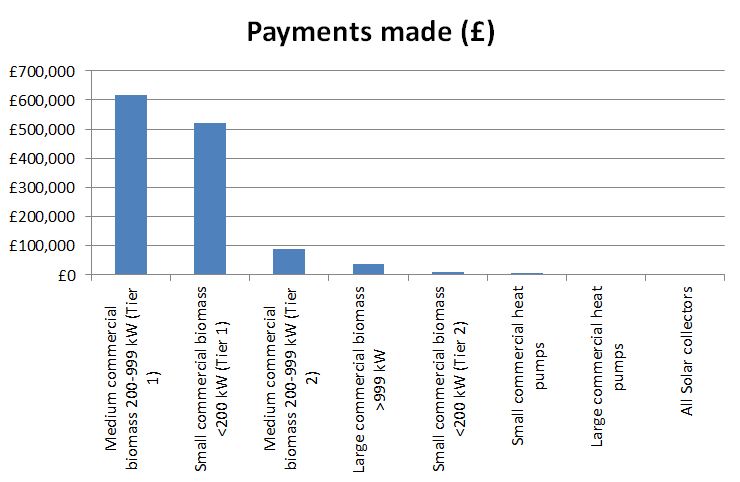

Biomass romps ahead

At 358 installations (commercial) biomass heating is leading the renewable heat scene at the moment. Based on our experience these installations are mainly to be found on farms and estates and often focus on a large property that is connected to multiple domestic and non-domestic properties in close proximity. We are also seeing smaller domestic systems that involve multiple dwellings connected to a single boiler.

|

| Date Source: Ofgem, 19/11/2012 |

Uptake in the new build/refurbishment sectors is happening, albeit at a much slower rate. While planning applications for large regeneration projects and new housing are coming through, particularly in the Growth Areas and Growth Points of Kent, the specification of biomass heating is rare, which seems odd given the interest from private finance houses in RHI-based investments and ESCo business models.

The integration of other renewable heat technologies alongside biomass does not yet appear to be common either. Even though solar thermal and biomass are best friends, to use a Jamie Oliver saying, we are yet to see it in action. This may be because of high capital cost of biomass which could be excluding secondary/complementary technologies (i.e. biomass is often sized to be as close to 100% of the heat load as possible with oil for peak which often makes the business case for complementary technologies less attractive).

Uptake in Kent?

Unfortunately the Ofgem statistics do not allow analysis at region or county levels. However, based on the work we are doing and the people we speak to, many of the large farm estates (particularly those with woodland interests) have made enquiries about the RHI and biomass technologies and several sites have gone ahead with projects.

|

| Kamstrup heat meter in action |

However, in the grand scheme of things uptake is still slow. We think that whilst interest levels are high the upfront capital cost of biomass remains the single largest barrier and prevents many from proceeding further. We know from the pre-feasibility studies we have carried out for people that the business case for biomass in the right situation is extremely compelling (i.e. 5 to 6 year payback, 10%+ return over the lifetime of the installation, 50% fuel cost reduction for wood chip).

|

| 650 kW Binder at Hever Castle |

Whilst we agree that biomass heating projects have a long lead in time, and take considerable project/business development, there may be a case for installing presenting finance options (if they have them) at a much earlier stage.

Domestic RHI on its way...

Don't forget that the purely domestic version of the RHI is being consulted on at the moment. This scheme is due to open in Q2 or Q3 2013. Our current thinking is that the tariff proposed for domestic biomass in the consultation is currently too low to make a significant difference in payback (and thus uptake). If you are interested in the RHI and are in a situation where you could qualify for the commercial RHI (e.g. 2 or more domestic dwellings connected to a single boiler) you may well be better off taking action now. We hope that the tariff under the domestic RHI improves and we will keep a keen eye on the consultation response by DECC.

Domestic RHI on its way...

Don't forget that the purely domestic version of the RHI is being consulted on at the moment. This scheme is due to open in Q2 or Q3 2013. Our current thinking is that the tariff proposed for domestic biomass in the consultation is currently too low to make a significant difference in payback (and thus uptake). If you are interested in the RHI and are in a situation where you could qualify for the commercial RHI (e.g. 2 or more domestic dwellings connected to a single boiler) you may well be better off taking action now. We hope that the tariff under the domestic RHI improves and we will keep a keen eye on the consultation response by DECC.

Can we help?

The Kent Downs Woodfuel Pathfinder can provide pre-feasibility support for people considering biomass heating. By 'pre-feasibility' we mean the assessment of viability and the development of an initial (non-market tested) business case. We can also support people as they engage with the installer network.

If you would any help with the RHI and biomass heating then please get in touch with us on 01303 815 171 or matthew.morris@kentdowns.org.uk.

Due to the way our project is funded our support needs to be provided mainly within Kent and should preferably link to woodfuel supply chains in/near the Kent Downs AONB. If in doubt just call!

No comments:

Post a Comment