Are you sitting comfortably?

DECC has been busy releasing new and updated information about both the commercial and domestic RHI and renewable heat in general.

To my eyes the overall renewable heat situation looks extremely healthy at the moment, particularly if you are in the biomass sector. However, it is also clear that biomass is dominating the commercial RHI. Consequently DECC will introduce changes to the budgetary process to increase the degression trigger sensitivity for sub-1MW biomass.

We have read the latest update on the commercial RHI and have picked out the main points from the executive summary. We would urge interested readers to look at the entire document in case we have missed anything.

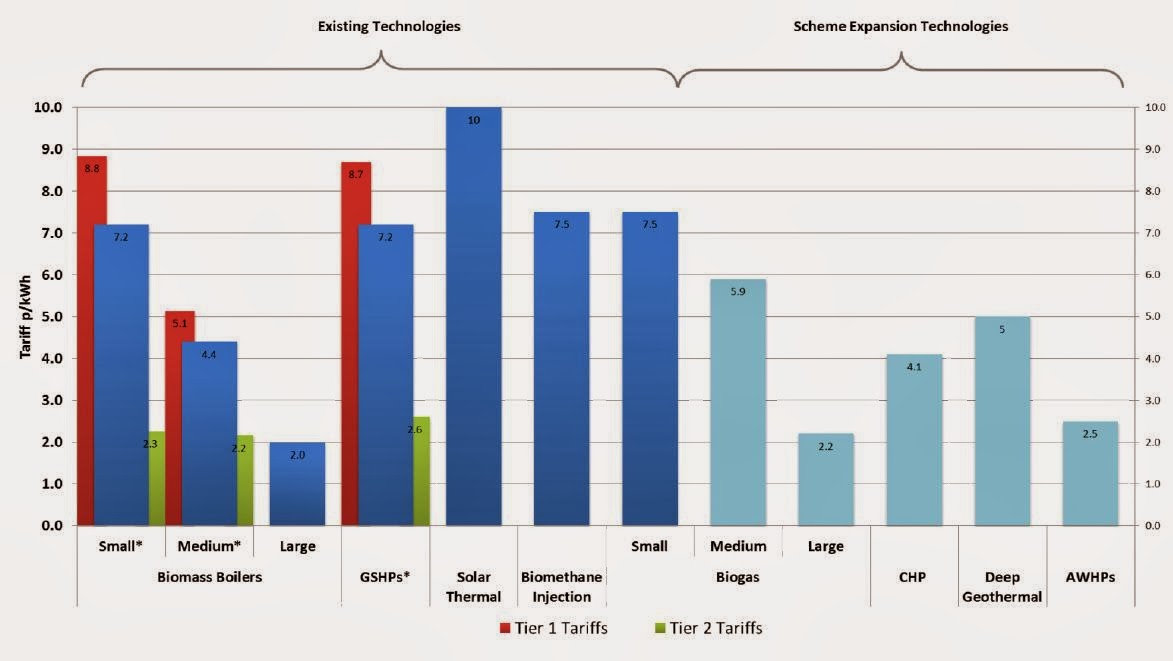

A key change is the capping of all tariffs at 10p/kWh. This means that the RPI inflation of tariffs will stop at 10p/kWh. For biomass it is the tier 1 small biomass tariff that is closest to this limit (n.b. the solar thermal tariff will be increased to 10p/kWh).

It is true that some renewable heat technologies are underperforming in the RHI, such as heat pumps and solar thermal. However, DECC has recognised this and will beef up support - via increased tariffs and budgets - as well altering some requirements (such as energy efficiency). The large biomass tariff, for example, will increase to 2.0p/kWh from 1.0p/kWh.

Eligibility

For new technologies and updated tariffs - 4 Dec 2013. Any applications with a date of accreditation of 21 January 2013 or later will benefit from the tariff increases brought forward as a result of the Early Tariff Review consultation (this applies to ground source heat pumps (GSHP), solar thermal and biomass over 1MWth).

Energy Efficiency

DECC will not be introducing explicit energy efficiency criteria for non-domestic RHI applicants at this time. The mixed views from consultation respondents made it clear that more work needs to be done to establish a range of effective but not unduly burdensome energy efficiency measures that could be introduced into the scheme.

Biomass Sustainability Update

Based on feedback from stakeholders about industry readiness, DECC will postpone implementing mandatory compliance with GHG lifecycle emissions savings to Autumn 2014, so that industry and participants can monitor their processes in light of the sustainability criteria and build the audit trail necessary to demonstrate compliance.

DECC intend for the Biomass Suppliers List to be open for applications from suppliers of biomass in Spring 2014.

Subject to the availability of Parliamentary time, DECC intend to implement land-use sustainability criteria by 1 April 2015.

Biomass CHP

DECC will be introducing support for biomass CHP (4.1p/kWh), biogas >200kW (5.9 p/kWh and 2.2pkWh depending on size) and deep geothermal (5.0p/kWh).

However, we do not intend to proceed at this time with support for heating only air-to-air heat pumps or biomass direct air as the consultation did not enable the development of appropriate deliverable policy.

Biogas combusion >200kWth

Subject to State Aid approval, tariffs will be set at 5.9p/kWh for installations with a thermal capacity of between 200 to 600kWth and 2.2p/kWh for those greater than 600kWth.

Deep geothermal

DECC will introduce a new tariff for deep geothermal heat at 5p/kWh. Deep geothermal heat will be defined as heat coming from a drilling depth of a minimum of 500m.

Heating only air-to-air heat pumps (AAHPs)

Although these technologies do produce renewable heat, DECC will not be introducing support for them at this time. This is primarily because of the risk of incentivising the installation of separate heating and cooling AAHPs in order to claim the RHI, rather than a reversible AAHP, which is likely to be more energy efficient.

Air to Water Heat Pumps and Energy from Waste

DECC will be introducing support set at 2.5p/kWh for AWHP (designed to achieve a minimum seasonal performance factor of at least 2.5) and 2.0p/kWh for the biogenic proportion of energy from waste (commercial and industrial).

Value for Money Cap and Tariff Rate of Return

From Spring 2014 tariffs across the RHI will be capped at 10.0p/kWh of renewable heat (and continue to be adjusted by RPI annually).

Biomass

To date deployment of large biomass has been below expectations and therefore DECC will go ahead with the proposed tariff increase to 2.0p/kWh.

Ground Source Heat Pump Tariffs

DECC will be replacing the current banded GSHP tariffs with a single tariff of 7.2p/kWh, which will be tiered.

The tier 1 tariff of 8.7p/kWh will be paid on the initial heat generated for an eligible purpose and the tier 2 tariff of 2.6p/kWh will be paid on the remaining eligible heat generated. This is equivalent to a tariff of 10.0p/kWh renewable heat assuming an SPF of 3.6.

Solar thermal

DECC will be raising the solar thermal tariff to 10.0p/kWh.

Budget management

Since implementation, DECC has made three quarterly degression assessments, one of which resulted in the medium biomass tariff being reduced by 5%. The outcome of the most recent assessment was published at the end of November. DECC will publish the fourth quarterly announcement by 1 March 2014.

In the May 2013 tariff review consultation we set out that the budget management policy would need to be developed in light of any tariff changes or scheme extensions and to reflect the outcome of the spending review for 2015/16, which has since confirmed an RHI budget in 2015/16 of up to £430m.

Having reviewed the budget management mechanism to ensure it remains fit for purpose, DECC will make some changes to the policy from Spring 2014 to:

DECC intend to introduce a form of tariff guarantee for the largest installations (for example, those over 1MW), initially available for plant due to be commissioned by 31 March 2016. Subject to further policy development in 2014, State Aid and Parliamentary approval, DECC will aim for this measure to be in place from April 2015 to March 2016 and thereafter factored into the next spending review discussions on the RHI so that it can be available from Spring 2016 for plant due to commission by 31 March 2020.

Public Grants

Public Grants

After two years of the non-domestic RHI we think a more flexible approach to the interaction between public grants and the RHI could encourage more renewable heat installations to come forward. Pending further work alongside the 2014 review to look at the interaction between public grants and the non-domestic RHI, DECC intend to introduce some additional flexibility next year. We will take forward regulatory amendments to extend the eligibility window for repayment of grants and to allow some grant recipients who are unable to pay back their grants to access the RHI via reduced tariff payments.

Energy Efficiency

DECC will not be introducing explicit energy efficiency criteria for non-domestic RHI applicants at this time. The mixed views from consultation respondents made it clear that more work needs to be done to establish a range of effective but not unduly burdensome energy efficiency measures that could be introduced into the scheme.

Biomass Sustainability Update

Based on feedback from stakeholders about industry readiness, DECC will postpone implementing mandatory compliance with GHG lifecycle emissions savings to Autumn 2014, so that industry and participants can monitor their processes in light of the sustainability criteria and build the audit trail necessary to demonstrate compliance.

DECC intend for the Biomass Suppliers List to be open for applications from suppliers of biomass in Spring 2014.

Subject to the availability of Parliamentary time, DECC intend to implement land-use sustainability criteria by 1 April 2015.

Biomass CHP

DECC will be introducing support for biomass CHP (4.1p/kWh), biogas >200kW (5.9 p/kWh and 2.2pkWh depending on size) and deep geothermal (5.0p/kWh).

However, we do not intend to proceed at this time with support for heating only air-to-air heat pumps or biomass direct air as the consultation did not enable the development of appropriate deliverable policy.

Biogas combusion >200kWth

Subject to State Aid approval, tariffs will be set at 5.9p/kWh for installations with a thermal capacity of between 200 to 600kWth and 2.2p/kWh for those greater than 600kWth.

Deep geothermal

DECC will introduce a new tariff for deep geothermal heat at 5p/kWh. Deep geothermal heat will be defined as heat coming from a drilling depth of a minimum of 500m.

Heating only air-to-air heat pumps (AAHPs)

Although these technologies do produce renewable heat, DECC will not be introducing support for them at this time. This is primarily because of the risk of incentivising the installation of separate heating and cooling AAHPs in order to claim the RHI, rather than a reversible AAHP, which is likely to be more energy efficient.

Air to Water Heat Pumps and Energy from Waste

DECC will be introducing support set at 2.5p/kWh for AWHP (designed to achieve a minimum seasonal performance factor of at least 2.5) and 2.0p/kWh for the biogenic proportion of energy from waste (commercial and industrial).

Value for Money Cap and Tariff Rate of Return

From Spring 2014 tariffs across the RHI will be capped at 10.0p/kWh of renewable heat (and continue to be adjusted by RPI annually).

Biomass

To date deployment of large biomass has been below expectations and therefore DECC will go ahead with the proposed tariff increase to 2.0p/kWh.

Ground Source Heat Pump Tariffs

DECC will be replacing the current banded GSHP tariffs with a single tariff of 7.2p/kWh, which will be tiered.

The tier 1 tariff of 8.7p/kWh will be paid on the initial heat generated for an eligible purpose and the tier 2 tariff of 2.6p/kWh will be paid on the remaining eligible heat generated. This is equivalent to a tariff of 10.0p/kWh renewable heat assuming an SPF of 3.6.

Solar thermal

DECC will be raising the solar thermal tariff to 10.0p/kWh.

Budget management

Since implementation, DECC has made three quarterly degression assessments, one of which resulted in the medium biomass tariff being reduced by 5%. The outcome of the most recent assessment was published at the end of November. DECC will publish the fourth quarterly announcement by 1 March 2014.

In the May 2013 tariff review consultation we set out that the budget management policy would need to be developed in light of any tariff changes or scheme extensions and to reflect the outcome of the spending review for 2015/16, which has since confirmed an RHI budget in 2015/16 of up to £430m.

Having reviewed the budget management mechanism to ensure it remains fit for purpose, DECC will make some changes to the policy from Spring 2014 to:

- base the deployment levels set out in the degression mechanism on refreshed market intelligence rather than the expectations that were modelled prior to the scheme’s introduction;

- reduce the tolerance in the technology trigger for biomass under 1MWth and bio-methane injection by reducing the amount that these triggers are scaled above expected levels of deployment. They will change from being 150% of expected deployment to 120% of expected deployment. This will reduce the risk of unsustainable growth and dominance of the budget by a small number of technologies;

- set the triggers for technologies DECC expects to deploy in relatively lower volumes (solar thermal, deep geothermal and all biogas) at 2.5% of the overall budget, rather than the current 5%.

DECC intend to introduce a form of tariff guarantee for the largest installations (for example, those over 1MW), initially available for plant due to be commissioned by 31 March 2016. Subject to further policy development in 2014, State Aid and Parliamentary approval, DECC will aim for this measure to be in place from April 2015 to March 2016 and thereafter factored into the next spending review discussions on the RHI so that it can be available from Spring 2016 for plant due to commission by 31 March 2020.

Public Grants

Public GrantsAfter two years of the non-domestic RHI we think a more flexible approach to the interaction between public grants and the RHI could encourage more renewable heat installations to come forward. Pending further work alongside the 2014 review to look at the interaction between public grants and the non-domestic RHI, DECC intend to introduce some additional flexibility next year. We will take forward regulatory amendments to extend the eligibility window for repayment of grants and to allow some grant recipients who are unable to pay back their grants to access the RHI via reduced tariff payments.

No comments:

Post a Comment