Defra's response to the Independent Panel on Forestry's report has been released and it makes interesting reading.

Defra's response to the Independent Panel on Forestry's report has been released and it makes interesting reading.

The Panel’s report has essentially led to a refreshed Government forestry policy. It will be based around a set of priorities: protecting, improving and expanding public and private woodland assets. It also reflects key Government principles, such as economic growth, localism, deregulation, targeted government intervention and value for money.

Of great interest to this blog is the announcement of an 'action plan' led by the wood industry that will consider, among other things, the important future role played by the biomass and woodfuel markets in the management of our woodland resource.

The main headlines from the response are as follows:

- The need to develop a new woodland culture and a resilient forestry and woodland sector,

- The value of the Public Forest Estate, which will continue to benefit from public ownership, be held in trust for the nation and be managed by a new, operationally-independent body,

- The importance of protecting our woodland assets,

- The need to bring more woodland into active management and increase the extent of woodland cover in England,

- The need to help the sector to find its voice and improve its economic performance,

- The importance of preserving and maximising the social and environmental benefits provided by trees and woodlands, particularly in and around our towns and cities,

- The scope for developing new markets based around a better understanding of the value and potential of our trees, woods and forests,

- The value of retaining a skilled cadre of forestry experts within the public sector.

Exploring New Opportunities: The role of woodfuel

Defra's response recognises that local renewable heat projects have the potential to provide an economic return to owners of even small areas of woodland and can benefit many businesses involved in the wider forestry sector:

- There are currently around 600 woodfuel supply outlets across Britain selling to local markets and there is potential to do more, provided this market is not developed at the expense of other wood processing industries and does not create unfair competition for our home grown products.

- Undermanaged broadleaved woodland in particular could supply significant quantities of fuel without interrupting current supply chains. More effective management of our woodlands will also make a long-term contribution to our challenging climate change targets, through reducing reliance on fossil fuels and energy intensive materials.

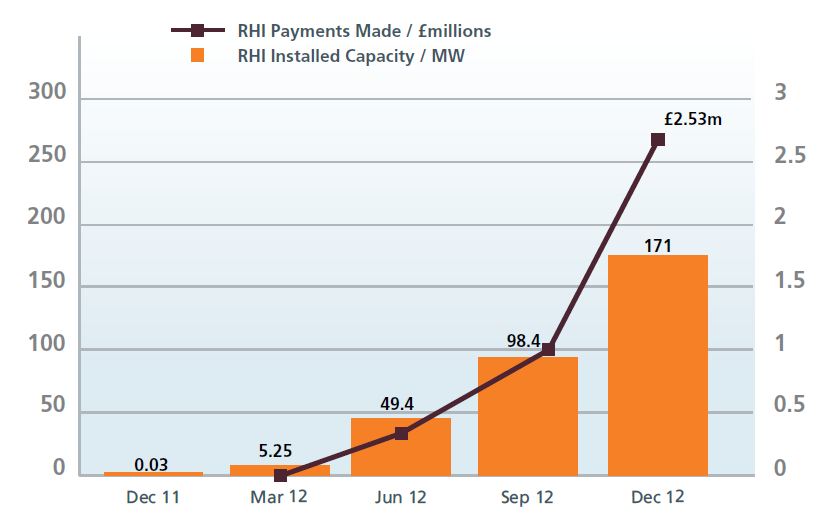

- With the introduction of the Renewable Heat Incentive the scope for developing new initiatives around woodfuel is growing.

To facilitate these objectives, the industry has invited Dr Peter Bonfield, OBE, Chief Executive of the Building Research Establishment (BRE), to lead the creation of a 'roadmap' (in autumn 2013) to a new and successful future for England’s forest-based supply chains.

This will be developed in partnership with woodland owners, managers, buyers, processors, researchers, retailers, contractors, woodfuel suppliers, community groups and Government.

Details of the organisations currently involved are on the Confor website.

A summary of the other main points are provided in the sections below.

Improving our Valuable Woodland Assets

This section of the response probably contains the most radical changes and clearly sets the policy towards economic growth:

- Work with landowners and others to increase the amount of actively-managed woodland and review progress in five years,

- Further reduce unnecessary regulation and red tape affecting the sector,

- Support the sector as it develops its new industry-led Action Plan,

- Work with the sector to explore the scope for exploiting economic opportunities, such as woodfuel markets and rural tourism,

- Encourage, where appropriate, local government and Local Enterprise Partnerships to take advantage of the opportunities provided by Government policies to realise the potential of local woodland assets.

Specific activities around people and communities and wildlife and the natural environment will continue.

Expanding our Woodland Resource

Increase England’s woodland cover significantly to achieve greater economic, social and environmental benefits:

- Deliver 12% woodland cover by 2060:

- Work with the sector to find new ways of encouraging landowners to plant more trees where it best suits them and their local conditions,

- Develop further the voluntary woodland carbon market and other sources of investment that reflect forestry’s low carbon credentials and wider public benefits to deliver a more wooded landscape,

- Pilot an initiative to reduce burdens on landowners who want to plant woodland by clarifying where a full Environmental Statement is unlikely to be required.

Protecting our Trees, Woods and Forests

Defra will give greater priority to tree and plant health. For example, the Living With Environmental Change (LWEC) Partnership will use £4 million of Defra funding, £0.5 million of additional Forestry Commission funding and up to £4 million additional funding from Research Councils to do in-depth research into tree diseases to inform the way outbreaks are handled in the future.

Governance and Structures

Defra plans to simplify current structures and step back from unnecessary day-to-day involvement:

- Retaining a core of forestry expertise within Government with the capacity to deliver a range of functions, duties and powers,

- Reviewing the Government’s forestry functions alongside the Triennial Review of the Environment Agency and Natural England,

- Working with the devolved nations to ensure that vital cross-border functions in areas such as research, standards and tree health can continue to be delivered centrally, where this is appropriate,

- Establishing via legislation a new, operationally-independent Public Forest Estate management body to hold the Estate in trust for the nation. It will be charged with generating a greater proportion of its income through appropriate commercial activity and with maximising the social, environmental and economic value of the assets under its care.

Realising More of our Woodlands’ Value

Defra acknowledges the social and environmental benefits of woodlands and to developing new market opportunities to realise these. Work already undertaken by the National Ecosystem Assessment, the Natural Capital Committee and the Ecosystem Markets will continue via:

- Working with the Natural Capital Committee and the Office of National Statistics to develop a set of natural capital accounts for UK forestry assets and use this to inform the development of a set of natural capital accounts for the Public Forest Estate,

- Developing a woodland ecosystem market roadmap to bring together actions by Government and our partners over the next 5 years to (a) build knowledge (b) develop wider networks of collaboration and expertise and (c) implement mechanisms and projects to demonstrate good practice,

- Working with others to support the further development of markets in forest carbon and other ecosystem services such as water and biodiversity.

We are hearing of reports from Trading Standards that some "rogue traders" are incorrectly advising householders that because of the ash dieback disease, the ash tree on their property must be felled or pruned.

We are hearing of reports from Trading Standards that some "rogue traders" are incorrectly advising householders that because of the ash dieback disease, the ash tree on their property must be felled or pruned.  Chalara dieback of ash, often referred to as ash dieback is a disease of ash trees caused by a fungus. The disease causes leaf loss and dieback in affected trees and depending on the age of the tree can lead to tree death. This BBC page is useful as an introduction to the subject.

Chalara dieback of ash, often referred to as ash dieback is a disease of ash trees caused by a fungus. The disease causes leaf loss and dieback in affected trees and depending on the age of the tree can lead to tree death. This BBC page is useful as an introduction to the subject.