The latest RHI figures continue to demonstrate how successful the scheme has been at increasing the rate of renewable heat generation in Great Britain.

Biomass heating remains the clear 'winner' of the RHI and account for 94% of all installations, 99% of the installed capacity and 85% of the payments made under the scheme.

Whilst the number of biomethane installations is small (just 3) they are starting to account for around 5.6% of the total payments made (which is great than the 'large biomass' category). As I stated before this seems to demonstrate the enormous potential of biomethane production from anaerobic digestion.

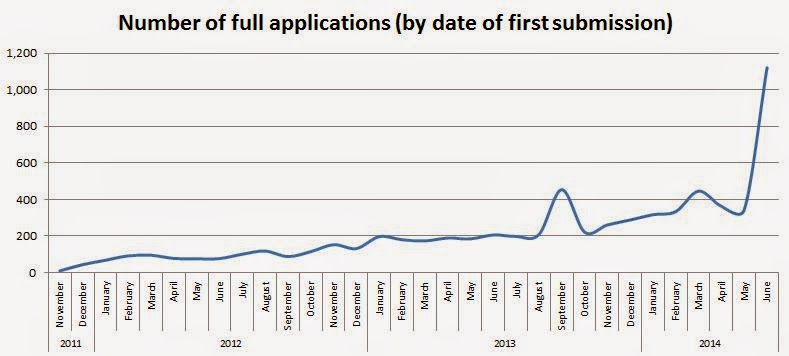

Of note, particularly to those considering installing a biomass system, is the recent acceleration in applications seen in June.

Whilst the precise reasons for this dramatic increase are not clear (backlog?) it is possible that it might lead to additional tariff adjustments later in the year (on top of the 5% reduction for small biomass implemented on July 1st).

In terms of geography the South West region continues to lead the way with 19% of all installations.

In the South East, where this blog lives, Kent has the most accredited installations.

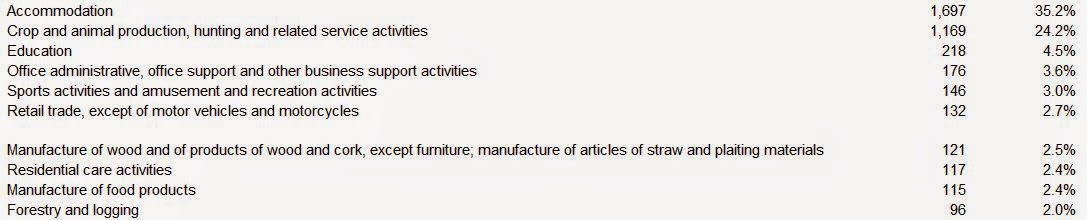

The top 10 business types benefiting from the RHI are shown in the table.

Will there be more tariff adjustments in 2014?

In simple terms - yes, quite likely.

The results of the next tariff review will be the announcement on 31 August 2014 (with any changes commencing on 1 October 2014).

The data suggests the expenditure thresholds for the overall RHI budget are starting to be exceeded. The cause of this is 'small biomass' tariff which is now well over its expenditure threshold.

This situation has been tolerated for a while because uptake of the non-biomass tariffs was, and still is, well below forecast and the overall budget was within its limits. The difference now is that uptake of the 'small biomass' tariff has accelerated so fast that it has now impacted the finances of the overall scheme.

Given the scale of the current overspend it is possible that a 10% reduction in the 'small biomass' tariff might take place on October 1st. This would reduce the tariff from 8.4 p/kWh (tier 1) and 2.2 p/kWh (tier 2) to 7.6 pence and 2.0 pence, respectively.

The impact of this reduction for a 199 kW biomass boiler is around £2,000 a year (although this depends heavily on the heat load and of course the actual meter readings).

Summary

There has been a large 'spike' in applications in June - whether this develops into a 'trend' is yet to be seen. Regardless of this the scheme overall is starting to overspend and as such the rules for degression are clear.

Any decision to reduce tariffs (in October) will most likely affect the 'small biomass' tariff.

Any sub-200 kW installations that are currently in progress now have a clear signal to complete as soon as possible. New projects, with an expected commissioning date post-October 1st, should probably factor-in a lower tariff for feasibility and business planning purposes.